We are experiencing an unprecedented event in our lifetime. However, that does not mean that this event will take down the global economy. Certainly, we will find that we will likely fall into another recessionary period in the coming months.

I have lived through almost 50 years of economic cycles. My father worked in a cyclical industry so the experience of economic ups and downs was learned by me very young and remains central in how I recommend developing financial plans. I remain very confident that we will persevere.

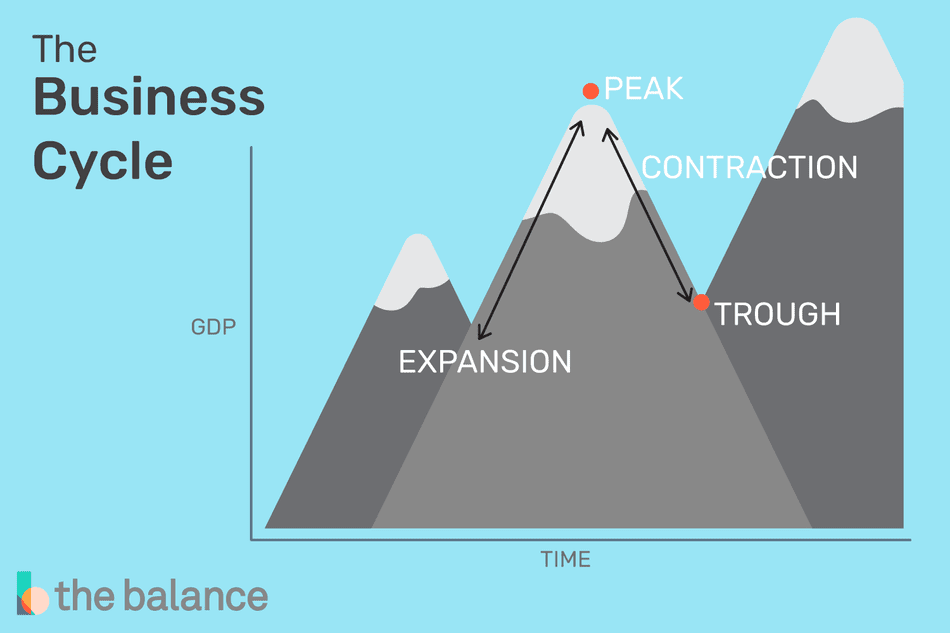

Economic cycles are normal but the catalysts for each recession is unique. Documented recessions began as early as 1785, following the American Revolution. Each recession has it’s uniqueness in causation, length and long term influences. However, the fact that humans adjust, strengthen and rebound is without a doubt. We can see evidence in sectors like medicine that will work to find solutions, government to help ease the economic effect and people to innovate and find ways to conquer and problem solve. Wikipedia has a nice history of U.S. recessions to help ease your mind that these events are normal and we will prevail. https://en.wikipedia.org/wiki/List_of_recessions_in_the_United_States.

How is Your Financial Plan Important to you Now?

The financial plan created for you needs to take into account your age, personal financial goals and cash flow needs. Your income needs during the next 5-7 year period need to be taken into account and balanced between short and intermediate-term investment needs. Your short-term money should be in the safest investment available for you. Your long-term investments should be invested in high quality, low cost investments. It is normal for these longer-term investments to experience ups and downs with the cycles in the economy. Therefore, those long-term monies are what you are seeing swinging during this volatile time. It does not feel good to see these accounts decrease in value, but this is necessary to experience the upside we have experiences the past decade. It is important to be able to work with an advisor that is familiar with economic cycles so they can best create and prepare an investment portfolio that will coincide with the stages of your life.

Cashing in in a volatile time, like we see today, can fail your long term plan. First, you will be selling at a low point, which will capture all the losses and limits long term growth. Secondly, the markets can swing quickly each day. Looking at the largest growth trading days, if you are out of the market on those days, your portfolio will miss capturing the abrupt upside potential, which will lower your overall growth potential. Historically, fear of the unknown will keep investors out of the market and cause them to miss the momentum of the upswing periods.

What is Important for You to do Now?

Being that we will likely see some very real economic hardships around the world, particularly within certain industries, we can prepare ourselves by making strategic decisions to take care of ourselves, our families and our goals. Here are a few ways I would recommend you take action

to help you persevere through this time and come out healthy and strong, both physically and financially.

- Take care of your body and health. Being sick affects your money. Healthcare costs will decrease money that can flow to other personal financial goals. Therefore, if you can, enjoy some fresh air, sunshine and healthy food to nourish your mind, body and soul. Use this period to slow down, enjoy yourself, your family and life. Decrease stress that you may be under as best you can. Stress reduces your immune system function, which increases the length and strength of any illness you may get.

- Look at your spending and see if there are any ways to build your savings account. Are there any “extras” that you can reduce during this time to build up your cash? If so, reduce those spending items and put the savings in your bank account. Building up your emergency money will help you face any extra expenses and/or decrease in income you may experience during this

- Pay down debt, starting with the highest interest rate debt you have. Work on changing your lifestyle to best align to your income and paying down debts owed. This will be important to long term wealth building and financial security through any economic cycle.

- If you are near retirement, make sure you have a solid financial plan before making your retirement decisions. Once you leave your job, a weak plan can cause your retirement income goals to

- Look at your job industry and see the outlook for job growth. Are there ways to prepare for opportunities and advancement for job security? Continuing educational skills will keep you as a top candidate to maintain jobs in a recession. In addition, being ahead of a downturn in your industry can help ward off being out of work. Begin career transition steps in the event your industry outlook is weak. The U.S. Bureau of Labor has a great resource to review the outlook of each industry. https://www.bls.gov/ooh/

- Look at your investment risk profile. This is not an ideal time to rebalance. However, think about your feelings about the ups and downs in the market. If you are panicked about the current market swings, we need to be sure we take those feelings into account as you decide your investment risk level. It’s easy to feel aggressive in an upswing market but not as easy to feel aggressive in 10-30% downswing periods in the market. Look at the long-term perspective, not the day to day shifts in the market. A few quick policy changes in the government or advances in medicine can quickly calm the market and cause an upswing. If you get out, you will get out for the ups too. Stay the course of your plan and keep a risk profile that is realistic for your

- Find a Fiduciary Financial Advisor. Ask lots of questions and make sure the Advisor is free from quotas, conflicts and able to provide you with a diverse offering of low-cost, quality investments at a fair price for their service. What type of company does the Advisor work for? An Independent Advisor can provide you with a more general offering vs. an Advisor that is tied to a particular insurance or brokerage company. What types of services does the Advisor give you for their fee? Fees will drag growth on your portfolio. Make sure the value you receive will offset the fee the advisor charges. Here are 10 questions to ask your planner. https://www.letsmakeaplan.org/blog/view/lets-make-a- plan-blogs/ten-questions-to-ask-your-cfp-professional

Wishing you great health, security and prosperity through these unknown and turbulent times. Written By,

Jennifer Hipkiss CFP®, EA, MSFP Fiduciary Tax & Wealth Advisor Main Office: (262) 465-6877

Email: JMHipkiss@hirep.net

Securities and advisory services offered through Harbour Investments., inc. Securities licensed in WI & CA https://harbourinv.com/clients/